Are Hedge Funds an “Asset Class?”

I’ve heard people refer to hedge funds as an “asset class,” implying that hedge funds are somehow distinct from other asset classes such as equities or fixed income. I believe that hedge funds are not a separate asset class but rather share similar investment attributes to the underlying assets they invest in.

Anticipate Distinct Outcomes

Regardless of where you come out on the issue, hedge funds are investment vehicles made up of distinct legal terms.

When a US investor buys a hedge fund interest, it’s typically buying a limited partnership interest or, if it’s a US tax-exempt investor, perhaps the interests in an offshore fund entity.

So while the investment attributes of, say, a long-short equity hedge fund may be highly correlated to the equity markets, the contractual terms of a hedge fund reflected in its limited partnership agreement may result in a much different investment outcome to investors based on a manager’s actions versus buying a basket of public equities.

Moreover, even among two or more hedge funds that pursue investment objectives with similar risk/return profiles, investors may experience different investment outcomes from one fund to the next, depending on what fund contractual terms permit mangers do or don’t do in pursuit of its investment program.

The Bottom Line

Be careful about applying labels to hedge fund investing that take into account strictly financial factors but ignore important contractual terms that can have a material impact on an investment outcome.

Lumping hedge funds together that have similar risk/return attributes and expecting similar investment outcomes can lead to disappointment if an investor is not aware of a fund’s contractual terms.

I want to highlight in this talk the importance of developing a legal framework to apply to the hedge fund investment process.

By framework, I’m referring to a set of legal factors that can be applied by investors and investment professionals to assess managers and hedge funds in a systematic way. A framework that can complement an investor’s financial analysis during the hedge fund investment process — both before and after an investment is made.

A hedge fund investment process that doesn’t take into account legal and regulatory factors, that relies strictly on financial factors to make investment decisions, is incomplete in my opinion. By not analyzing legal and regulatory factors associated with a hedge fund investment or its manager, the risk of investment loss may be greater and investor bargaining power is diminished.

Or consider an investment professional managing money for an individual, family or entity. If that investment professional is considering making a hedge fund investment on behalf of its client and he or she doesn’t consider legal and regulatory issues associated with an investment, has that person met his or her fiduciary and/or other duties to its client? These issues are a big deal.

Avoid the Reactive Approach

The legal profession, in my opinion, has not supplied investors and investment advisors with an analytical framework with which to analyze hedge fund investments during the investment process.

To the extent that the lawyers address the concerns of hedge fund investors in any consistent way, they tend to address investment process issues in a piecemeal way.

The existing legal approach is often reactive as opposed to proactive (issues are discussed based on some headline risk that’s in the news at a particular time) and it doesn’t provide investors with a framework that they can apply consistently to consider and screen different investments. I think that’s a failure.

Why?

Because this approach fails to take into account the way that most successful investors that I know go about investing. The process that they rely on often involves the application of a consistent set of financial or investment beliefs that is utilized to help evaluate and screen potential investments and monitor and dispose of them once an investment has gone through.

Investment vs. Legal Framework You can be a value investor, a distressed investor, a growth investor, use technical or fundamental analysis, believe or not believe in efficient markets, whatever. I’m not making any judgments as to the merits of any particular investment style or whether it will or won’t make money.

It’s only to note that investors often apply an analytical investment framework to screen investments based on certain quantitative and qualitative principles.

And yet, when they look to lawyers to help analyze factors associated with the hedge fund investment process in some systematic way, they’d be hard-pressed to find such an approach.

That’s ironic because this is an area that has gotten a lot of good work done in it over the years by regulators like the SEC.

Legal and regulatory issues associated with investing in a hedge fund shouldn’t be opaque or require an investor to have to “reinvent the wheel” each time.

In these talks, I’ll build a legal framework associated with the process of hedge fund investing and try to fill that gap. A legal framework should strive to be efficient, comprehensive and consistent in its application across many different hedge funds and that’s what I’ll aim for.

The Importance of Incentives There are two concepts that I’ll highlight in this talk. First, the importance of incentives in influencing behavior in the hedge fund context. Second, the process of backward thinking to identify legal risks with hedge fund investing. I associate both points with Charlie Munger.

Munger is, of course, Warren Buffett’s longtime investment sidekick. Prior to hooking up with Buffett, Munger was a successful investor in his own right and was trained as a lawyer.

Like Buffett, he’s given a lot of thought over the years to developing good mental models for decision making. Like Buffett, he’s been willing to share those thoughts in speeches and writings that I’ve found useful.

“Never, ever, think about something else when you should be thinking about the power of incentives.”

— Charlie Munger

Munger’s quote should be considered a cornerstone of any legal framework focused on hedge fund investing.

In my opinion, the power of incentives to influence manager and investor behavior in the hedge fund context cannot be overstated enough.

More than any other investment vehicle that I’m aware of, hedge funds are engineered to permit managers maximum behavioral flexibility based on changing circumstances faced over the life of a fund. The incentives that can influence their behavior are embodied in a fund’s legal terms.

That may not be a bad thing in certain cases.

However, if an investor or its adviser choose to ignore the influence that legal terms have in defining a manager’s incentives and thereby potentially shaping future action, they do so at their own peril.

So it’s important to analyze hedge fund legal terms in how they may influence incentives and future behavior, not as an academic exercise.

The second point I want to discuss here is the process of analyzing a hedge fund’s terms by employing a technique of inversion or thinking backwards about what can go wrong once a desired investment outcome is determined.

Thinking Backward “A lot of success…in business comes from knowing what you really want to avoid” — Charlie Munger

What are your hedge fund investment goals? Let’s flip that question: What do you want to avoid? Obviously investment loss is one. How about excessive fund expenses? Fund proceeds that are locked up? Onerous indemnification claims or conflicts of interest?

There’s a terrific book that I recommend called “Seeking Wisdom: From Darwin to Munger” by Peter Bevelin. It focuses on practices to improve critical thinking based on the works of Munger, Buffett and many others.

There’s a section in the book called “Guidelines for Better Thinking” and it lists 12 principles.

Number 10 is “Backward Thinking” which we can define as the process of starting with an end goal in mind and working backwards to identify everything that can go wrong with the achievement of that goal as a means of identifying risk.

Using that technique, once we have a clear investment goal in mind and work backwards to identify factors that can mess up that desired outcome, we can make an assessment as to whether those factors are ones that:

1) we can live with,

2) seek to modify or

3) simply avoid.

Title Slide: Risky Business Why is this method important to identify legal and regulatory risk associated with hedge fund investing?

Because a lot of risk associated with hedge fund investing beyond the investment risk lies buried in the documents. It’s the latent contractual terms and provisions that can spring to life if certain conditions are met.

Hedge fund documents are often dense and loaded with terms and provisions that may have no applicability at any one point in time. They may look innocuous.

The problem is that it’s often difficult to properly assess those risks if an investor focuses its analysis strictly at the front end of the hedge fund investment process when an investment is made.

Also, hedge fund documents may not address certain risks that an investor considers material to a desired investment outcome. So it’s important to review those documents not only for what’s in them but also what’s not to properly assess risk.

By defining the investment end-goals first and thinking backwards, a person is better able to review the terms of a hedge fund’s legal documents to determine what in the documents can mess up that desired outcome and any gaps that should be addressed.

Once identified, sensitivity analysis can be done on those terms to determine whether an investor with a desired investment outcome can live with a specific term, seek to modify it or simply not make the investment.

Next Up Throughout our talks, we’ll go through a process of inverting our thoughts with respect to different hedge fund legal terms and couple that process with a focus on the power of incentives to assess legal and regulatory risk.

Next we’ll turn to defining what a hedge fund starting with a “top down” approach.

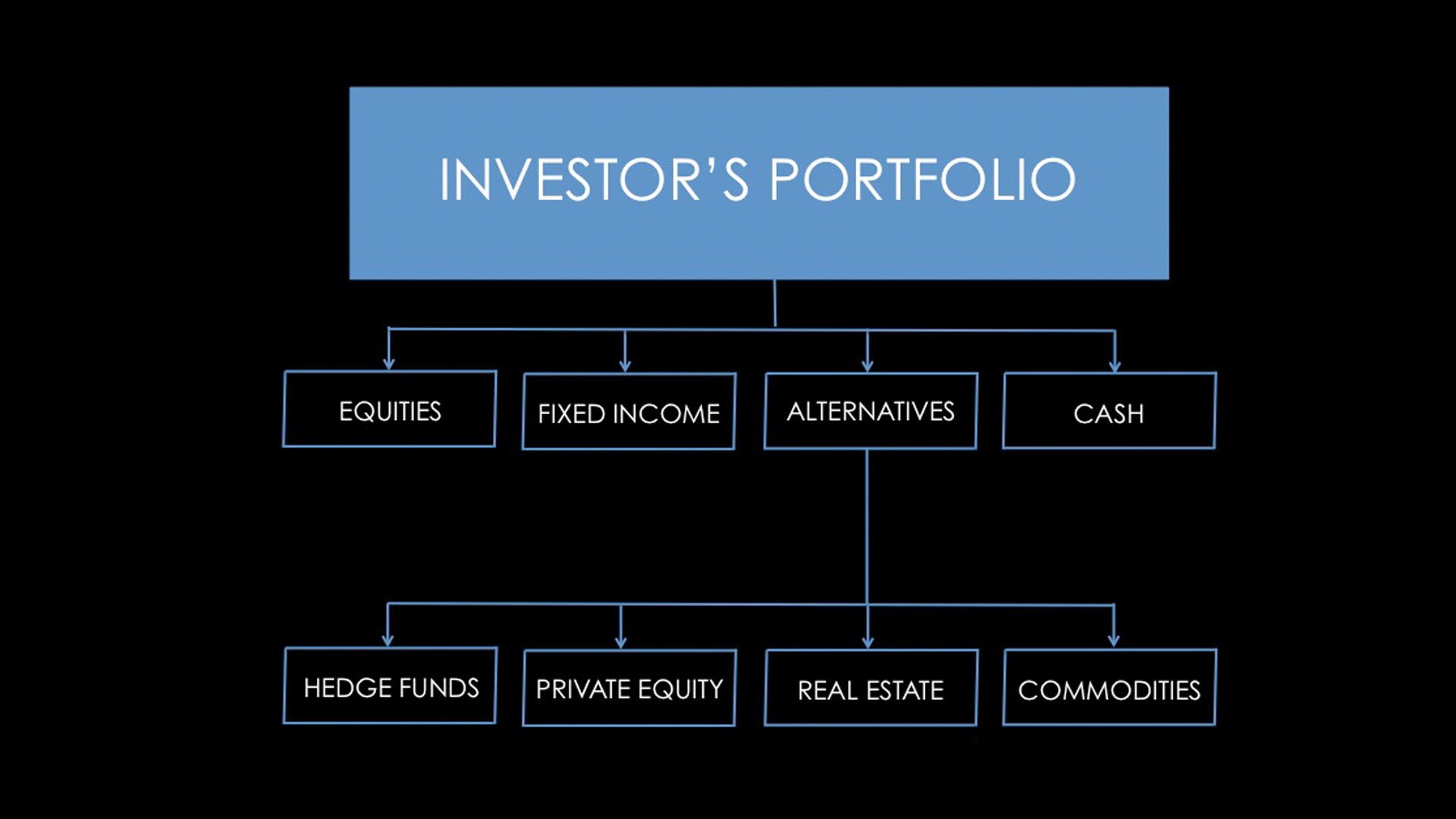

Top Down Approach Let’s start to define what a hedge fund is using a “top down” approach. We’ll look at hedge funds at an investor’s overall portfolio level and highlight some background information. Then we’ll get granular on what a hedge fund is.

This is a typical investment portfolio that an institutional or high net worth investor manages. It usually consists of seven broad investment categories or what some folks call “asset classes.”

These seven categories include “traditional” investments (equities, fixed income and cash) and what’s referred to as “alternative” investments (hedge funds, private equity, real estate and commodities).

I’ve simplified things here for illustrative purposes and haven’t included things like venture capital which, when compared to the total assets invested by investors into hedge funds or private equity, is often negligible.

Depending on where we are in the economic cycle and where attractive investment opportunities are present, investors and their investment professionals will shift money among these different investment categories or “reallocate” assets from one category to another to meet their investment objectives.

Key Trends In the US, one of the important portfolio management trends we’ve seen over the last 15-20 years by large investors is a significant increase in alternative investments.

20 years ago, a large investor might have allocated 10 or 15% of its overall portfolio to alternatives investments, usually consisting of real estate and some small percentage of private equity investments.

Today that figure is often much higher, with some large investors allocating as much as 50% of their aggregate portfolio assets into alternative investments including hedge funds.

In the case of hedge funds, the rise in assets and managers has been very dramatic. Today there’s close to $3 trillion dollars being managed by hedge funds globally based on the numbers I’ve seen and, as of September, 2014, there were roughly 2,700 managers that were registered with the SEC that managed at least one hedge fund (and that doesn’t include US and foreign hedge fund managers that for whatever reason weren’t required to be registered with the SEC).

The reasons for this portfolio shift towards hedge funds and other alternatives includes a desire by many investors to try to find “uncorrelated” returns among their different portfolio investments coming off the equity market meltdown in 2000 and the overall market collapse during the 2007-2008 Credit Crisis.

Ownership of these different investment categories often takes one of two forms: An investor either owns a particular asset directly or through some fund entity such as a hedge fund that pools money from different investors and is managed by an investment manager for fees.

Important Consideration An important consideration with respect to any investment fund is whether that fund is required to be registered with the SEC under a federal securities statute called the Investment Company Act of 1940.

Generally if a fund is required to be registered under the Investment Company Act, it will be subject to restrictions on its operations and its use of certain portfolio management techniques such as leverage.

As its name implies, a hedge fund is a pooled investment vehicle that typically consists of multiple investors and is advised by an investment manager.

Unlike a mutual fund, managers avoid registering hedge funds under the Investment Company Act and thereby avoid the operational and investment restrictions that the statute imposes.

That’s important because hedge fund managers often seek to employ portfolio practices to make money that can’t be limited by any statutory restrictions.

Managers are able to avoid having to register their hedge funds under the Investment Company Act by complying with various private placement rules. They sell hedge fund interests to institutional and high net worth investors that meet certain net worth standards under US securities laws.

Investor Eligibility There are various “high net worth” tests to determine whether an investor is eligible to buy a hedge fund interest in a private placement.

One popular standard that managers use is the “qualified purchaser” standard, which generally means that individuals must have a minimum of $5 million of investable assets and institutions $25 million in investable assets to be eligible to invest in certain hedge funds.

Because hedge funds aren’t registered under US security laws and their interests are privately placed, you’ll often hear lawyers often refer to them as “private funds.”

The combination of hedge funds not having to register with the SEC as registered funds and their interest being sold pursuant to US private placement rules has important implications for the investment process that we’ll return to in future talks.

In a speech delivered today entitled “Conflicts, Conflicts Everywhere,” Julie Riewe (Co-Chief of the SEC’s Asset Management Unit – Division of Enforcement), highlighted her group’s “overarching concerns” about manager conflicts-of-interest issues across different investment vehicles including hedge funds and private equity.

Key Quote

“Over and over again we see advisers failing properly to identify and then address their conflicts.”

Background One of the most important principles guiding the U.S. asset management industry (including alternative investment managers) is that managers should assiduously avoid conflicts-of-interest practices that place their interests ahead of their clients in managing money. Over the years, the SEC has identified many practices that raise conflicts-of-interest concerns and has adopted an extensive regulatory regime to ensure that managers address and correct these concerns where necessary. Key is the notion that managers identify conflicts-of-interest issues to their clients and fix them where necessary.

Conclusion Ms. Riewe’s speech identifies specific areas of anticipated SEC enforcement action against managers involving conflicts-of-interest matters (see below). These areas provide investors with valuable guide posts to consider related to their own due diligence procedures to identify potential conflict-of-interest issues associated with managers and alternative investment vehicles. In my opinion, broad, generic conflicts-of-interest disclosure that can be so typical of private fund offering memorandums often doesn’t cut it. A manager should provide investors with detailed conflicts-of-interest disclosure that is specific to its investment program, operations and overall business.

Anticipated SEC enforcement action will include:

A) Conflicts-of-interest matters to be brought against managers

Best execution failures in share class context

Undisclosed outside business activities

Related party transactions

Fee and expense misallocation issues in the private fund context

Undisclosed bias toward proprietary products and investments

B) Specific for private fund managers

Undisclosed fees (hedge funds)

All types of undisclosed conflicts, including related-party transactions (hedge funds)

Valuation issues including use of friendly broker marks (hedge funds)

Undisclosed and misallocated fee and expense cases (private equity)

An important consequence of a manager registering with the SEC is that it becomes subject to the SEC examination process. SEC examinations are conducted to ensure that registered managers comply with the various federal rules and regulations that govern their business. The SEC has ramped up the resources and expertise it’s dedicated to this activity in recent years.

SEC-led examinations of registered managers can be very thorough. They often uncover “deficient” areas related to a manager or its operations that may be difficult for investors to discern given the limited amount of manager-related information that investors may have access to.

The problem areas identified by the SEC are usually addressed in correspondence between the SEC staff and a manager for follow-up action. The process is confidential but that does not preclude a manager from voluntarily sharing the results of any SEC examination with its investors.

The issues identified by an SEC exam can be relatively innocuous or more serious. However, since beauty is often in the eye of the beholder, an issue that one investor may consider innocuous, another may consider more serious. That’s an important judgment call for each investor to make. Inquiries by an investor to a manager on the results of any SEC examination done prior to a private fund investment, and, on an ongoing basis once an investment is made, is an important investor due diligence tool.

This is a busy time for many SEC registered managers related to disclosure requirements. SEC registered managers are required to file updated Form ADVs with the SEC within 90 days of the fiscal year-end (March 31 deadline for managers with a December 31 fiscal year-end).

Managers provide portions of their updated Form ADVs to investors in private funds within 120 days of the fiscal year-end.

The timing of SEC disclosure requirements means that certain fund investors may not receive updated information on a manager, its personnel, operations or investment products until well after a change has occurred. Form ADVs being reviewed by investors that are close to a year old and have not been amended may contain stale information.

A manager must also determine whether the changes reflected in its amended Form ADV filed with the SEC will require updates to their fund’s offering documents. Maybe, maybe not. That’s a judgment call that a manager will have to make. Suffice it to say that nasty surprises can occur if an investment is made before a manager shares updated information with regulatory authorities and investors.

Be aware of these SEC deadlines. If a manager hasn’t updated its Form ADV and an investment is being contemplated during this 90-day amendment period, consider inquiring:

1) when the manager anticipates making its amended Form ADV filing;

2) whether the manager is currently aware of material changes that will be reflected in its future Form ADV filing; and

3) whether fund offering documents will also have to be updated to enable an investor to make an informed investment decision.

A prospective investor to a private investment fund will likely be asked to sign a confidentiality agreement by a manager early in the investment cycle. These contracts are typically presented as “off-the-shelf” forms by managers. A confidentiality agreement can be one-sided when first presented and commit a prospective investor to ongoing obligations even if they do not invest in a fund. Based on my experience, here are ten one-sided conditions related to confidentiality agreements that investors should be aware of:

1. Definition of confidential information is overly broad

2. Agreements are open-ended with no termination date

3. Contract terms conflict with confidentiality provisions in fund documents

4. Limitations on investor’s ability to share information with advisers

5. Exceptions to confidential information are too limited

6. Manager exculpation clauses on information provided don’t account for anti-fraud concerns

7. Contract terms interfere with investor’s ability to respond to legal matters unencumbered

8. Onerous choice of law provisions

9. Investor unfairly responsible for ongoing expenses

10. Agreements lack basic contractual clauses (e.g., amendments, entire agreement)

In Part II of our video series, Yarden Law Founder Nir Yarden provides insights on the investment process including a quote from Eugene Fama. Key discussion points include the ability of legal factors to add certainty to an uncertain hedge fund investment process and navigating investment risk management.

We kick off a new video series: “The Process of Hedge Fund Investing.” In Part I, Yarden Law Founder Nir Yarden describes his background, along with the importance of filling a critical legal void for investors.